NEWS

Monday 9 July 2018

As most readers will be aware, at MAXIS GBN, we are a passionate advocate of the use of captive reinsurance companies to help multinational businesses better administer a global risk management programme.

But why are we so in favour of them?

In many instances, if managed successfully, multinationals can realise global cost savings through reduced risk charges and administration fees. In addition, in terms of enhanced benefit design and policy terms such as exclusions, free cover limits and event limits, establishing a captive employee benefits programme enables a business to improve control over benefits programmes globally while increasing flexibility in plan design along with policy terms and conditions.

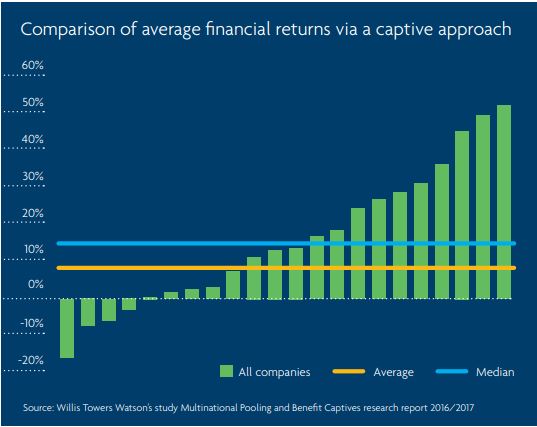

Willis Towers Watson’s study Multinational Pooling and Benefit Captives research report 2016/20171 examined the performance of multinational pooling and employee benefits captive arrangements. The study found average dividend returns for multinational pools of 6%, with top quartile results producing dividends of over 14%. For employee benefits captives it identified the savings could be even greater, with median surpluses of 15% and the top quartile producing 25% or more.

Some captive arrangements delivered even higher returns because companies actively discounted premiums up-front, before reinsuring them to their captives. Among other points, Willis Towers Watson’s study stated that life insurance contracts were the most consistently profitable, with returns of nearly 27% for employee benefits captive business.

While the size of the employee benefits captive market remains small in comparison to the Property and Casualty (P&C) captives sector, there is clearly an increasing appetite from multinationals to explore the rewards that captives bring when reinsuring employee benefits programmes in terms of control, governance, cost reduction and data strength.

Health and well-being programmes coming to the fore

Health and well-being programmes coming to the fore

Consequently, multinationals are looking at ways to break this trend of increasing claims and medical cost inflation, which helps explain why health and well-being programmes are now so prominent and increasingly command significant investment. Captive structures are playing their part by centralising underwriting processes and allowing much greater control from HR and risk teams.

At MAXIS GBN, we have been at the forefront of providing clients comprehensive data that allows for a deeper understanding of cost drivers. With MAXIS Global Wellness recently launched, we are aiming to meet the demand from multinationals for further analytics that can support the implementation and optimisation of effective health and wellness programmes.

The use of captives to manage pension liabilities continues to be a topic of interest, albeit still only really relevant to a select set of clients and multinationals. Of course, the de-risking of defined benefit pension schemes has been a strong focus over the past decade, yet a number of companies still find that captives can help them to optimise their strategy, either by pooling their pension assets or by calibrating the biometric and or financial risks they are willing to take on their books. This is supported by an increasing availability of financial instruments that allow for such calibration.

We are fortunate that AXA, one of our two parent companies, along with MetLife, is at the forefront of this market.

“… the majority of risk managers have a P&C background... This poses interesting challenges to common employee benefits structures.”

The increasing role risk managers are playing in managing employee benefits

One of the drivers behind this market activity is the increased role risk managers are playing in managing employee benefits. Once the preserve of the HR function, employee benefits are more and more often coming under the remit of risk and finance functions. This is due to the growing need to govern employee benefits lines financially, including being able to gain access to underwriting profits. The development of this approach has accelerated ever since the 2008 financial crisis.

Naturally, the majority of risk managers have a P&C background and it is apparent that many are seeking to apply common P&C approaches to the employee benefits space. This poses interesting challenges to common employee benefits structures.

Another trend that is reinforced by rising costs for letters of credit and the current low interest environment, is the way in which clients wish to reinsure their employee benefits risks to their captive. Traditionally, a key reason for implementing an employee benefits captive was to hold the assets required for the delivery of the benefits programmes at a later date.

Recently, however, a growing number of clients are preferring to work on a funds-withheld basis, which allows for lower collateral requirements. This is because the reduction in costs for maintaining collateral can outweigh the expected higher returns on investment holding assets within the captive. This preference could, of course, change once interest rates rise, which is what many economic commentators are forecasting.

“For employee benefits captives… savings could be even greater, with median surpluses of 15% and the top quartile producing 25% or more.”

We believe that, overall, by using captives to manage employee benefits risks, multinationals benefit in three ways. Firstly, they are retaining the underwriting profit for themselves. Secondly, they can capitalise on the diversification benefits that this brings, employee benefits are higher frequency, lower impact compared to P&C risks and represent a welcome diversification for risk managers.

Finally, by centralising processes they are getting much more control of their employee benefits programmes something that HR, risk and finance teams greatly appreciate. And that’s why, at MAXIS GBN, we believe in Captives.

If you have any questions about Captives don’t hesitate to get in touch.

1 https://www.willistowerswatson.com/en/press/2017/03/Multinational-Pooling-and-Captives-increasingly-used-to-limit-cost-of-insurable-employee-benefits

2 http://www.aon.com/2017-global-risk-management-survey/pdfs/2017-Aon-Global-Risk-Management-Survey-Full-Report-062617.pdf

The MAXIS Global Benefits Network (“Network”) is a network of locally licensed MAXIS member insurance companies (“Members”) founded by AXA France Vie, Paris, France (AXA) and Metropolitan Life Insurance Company, New York, NY (MLIC). MAXIS GBN, registered with ORIAS under number 16000513, and with its registered office at 313, Terrasses de l’Arche – 92 727 Nanterre Cedex, France, is an insurance and reinsurance intermediary that promotes the Network. MAXIS GBN is jointly owned by affiliates of AXA and MLIC and does not issue policies or provide insurance; such activities are carried out by the Members. MAXIS GBN operates in the UK through UK establishment with its registered address at 1st Floor, The Monument Building, 11 Monument Street, London EC3R 8AF, Establishment Number BR018216 and in other European countries on a services basis. MAXIS GBN operates in the U.S. through MetLife Insurance Brokerage, Inc., with its address at 200 Park Avenue, NY, NY, 10166, a NY licensed insurance broker. MLIC is the only Member licensed to transact insurance business in NY. The other Members are not licensed or authorised to do business in NY and the policies and contracts they issue have not been approved by the NY Superintendent of Financial Services, are not protected by the NY state guaranty fund, and are not subject to all of the laws of NY. MAR00266/0718