NEWS

Wednesday 7 October 2020

Employers all over the world are investing vast amounts of money on insured employee benefits (EB) in an attempt to take the best care of their most valuable asset – their people. It comes as no surprise, therefore, that multinationals are always looking for the most cost-effective financing strategies for their EB programmes, enabling them to offer the right benefits, to attract and retain the best talent, while ooking after their budgets.

Global underwriting programmes, or global risk solutions (GRS) as we call them, have become increasingly popular in recent years and are now often talked about as an alternative to traditional multinational pooling and the more modern captive structures. But are they a viable solution for managing EB costs for multinationals?

How does a GRS differ?

For many businesses and multinationals, a global pool will be the right option for managing their EB programme and they may never need to move to a different solution. For the largest businesses, a captive programme can bring the greatest rewards by putting them in control of their global EB programme, but it requires real commitment as they will ultimately be holding the risk.

And while pools and captives remain the most common ways to manage EB risks, GRS has become a compelling option for large, centralised multinationals spending multimillions each year on insurable employee benefits. The solution enables employers to place several local employee benefits programmes with one EB network to form a programme underwritten at the global level.

As the portfolio is underwritten this way, and involves a multi-year commitment, GRS programmes can provide upfront break-even portfolio level pricing and improved terms and conditions, with attractive rate guarantees on select benefits.

GRS has become a compelling option for large, centralised multinationals spending multimillions each year on insurable employee benefits.

GRS at a glance

The benefits

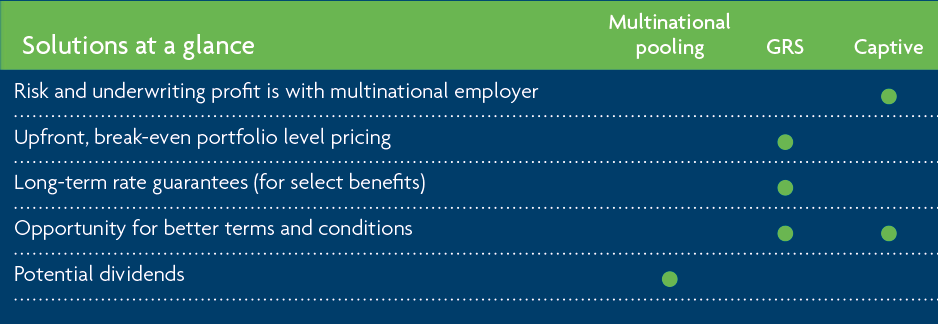

- Upfront, break-even portfolio level pricing

- Long term rate guarantee on select benefits (typically three years)

- Improved terms and conditions

- Stronger global governance

Who is it right for?

- Large multinationals with centralised employee benefits

- Multi-million currency EB portfolio

- At least three years of EB data

The keys to a GRS – size and data!

It all sounds very positive, so why doesn’t everyone use a GRS to finance their employee benefits? It’s really a question of size and data-centralisation is also important but more on that later. A global pool can typically be set up with 10% of the premium volume that’s needed for a GRS programme to be effective – so only large companies are really set up for a GRS. Because the portfolio is underwritten globally, GRS programmes need this premium volume to offset the potential volatility in any one market.

Advances in data capture and analytics which allow for more detailed and accurate analysis of risks across individual markets have made it possible to underwrite a global portfolio like this. This ability to project the outcomes – and price the risk – of a multi-year programme means that multinationals can be given better pricing in advance.

That’s why data is key for a GRS – without at least three years of claims experience on the portfolio it’s more difficult for global benefits networks to accurately project claims and offer the competitive upfront rates and guarantees that make these programmes so enticing for multinationals.

It’s vital to understand, at an in-depth actuarial level, the premiums and claims experience by each line of product in each country. Not all companies have this degree of centralisation and this quality of data.

Matthias Helmbold, Head of Technical & Services at MAXIS GBN, says: “Pooling can often meet the needs of most large companies and GRS programmes aren’t suitable for everyone. But for centralised multinationals who have the premium volume and historic underwriting data, it’s an exciting prospect and can be very beneficial. They don’t need local market pricing reviews, and they can achieve stronger global governance and embed their global benefits strategy, while ensuring they have sustainable pricing.

“For businesses looking to start a GRS programme, there are two key considerations. The solution only works if there’s a substantial amount of business that we can bring together and effectively underwrite. Also, multinationals and their partners should look at this as a long-term solution, often over three-years at the very least. The pricing and rates reflect a deeper commitment and a more partnership-like approach.”

That’s why data is key for a GRS – without at least three years of claims experience on the portfolio it’s more difficult for global benefits networks to accurately project claims and offer the competitive upfront rates and guarantees that make these programmes so enticing…

Key differences: pooling, GRS and captives

Pooling – a global pool can give a multinational employer a potential profit-share payment or dividend if the aggregate results of their life, accident, disability and medical policies in their pool provide a positive year-end portfolio balance in their annual report.

Pooling – a global pool can give a multinational employer a potential profit-share payment or dividend if the aggregate results of their life, accident, disability and medical policies in their pool provide a positive year-end portfolio balance in their annual report.

GRS – this solution allows benefits to be underwritten at the global level. Unlike pooling, this is a longer-term commitment (a minimum of three years) , that requires a high degree of centralisation and usually has a larger portfolio. Historic underwriting data covering a period of three years or longer is important to effectively underwrite the programme at break-even pricing.

GRS – this solution allows benefits to be underwritten at the global level. Unlike pooling, this is a longer-term commitment (a minimum of three years) , that requires a high degree of centralisation and usually has a larger portfolio. Historic underwriting data covering a period of three years or longer is important to effectively underwrite the programme at break-even pricing.

Captives – a captive is usually the best way to finance global programmes for the largest multinationals. A captive allows the risk from local life, accident, disability and medical policies to be passed to a multinational employer’s captive (re-)insurance company. The captive will get the benefit of the underwriting profit (a major advantage of captives), along with the opportunity to improve terms and conditions and have greater flexibility in the design of their benefits plans.

Captives – a captive is usually the best way to finance global programmes for the largest multinationals. A captive allows the risk from local life, accident, disability and medical policies to be passed to a multinational employer’s captive (re-)insurance company. The captive will get the benefit of the underwriting profit (a major advantage of captives), along with the opportunity to improve terms and conditions and have greater flexibility in the design of their benefits plans.

GRS – a collaborative partnership

GRS – a collaborative partnership

Partnership is an absolutely key concept when it comes to GRS. Firstly, within the multinational itself. Without a strong relationship between HR, finance, risk and procurement functions at the global level, the multinational won’t be centralised enough to run a successful GRS programme. There also needs to be a strong collaborative framework in place between the global head office and local HR functions, so they are aware of the benefits on offer and follow the correct process for EB.

Multinationals can work with global brokers or consultants who can help to put these governance structures in place to oversee and control the programme. Without effective centralisation and governance, global risk

programmes can fail to meet expectations – or even fail altogether.

And as Matthias Helmbold said, it’s important to work closely with the EB network running the GRS. As this is a longer-term programme, the network needs to work closely with both the multinational and broker or consultant to help the programme achieve success.

Without effective centralisation and governance, global risk programmes can fail to meet expectations – or even fail altogether.

A GRS success story

Here’s an example of how one multinational client has had success with a GRS programme.

The details?

The client has a history of using a GRS to finance EB but has used its current programme since 1 January 2013. This GRS is predominantly for medical insurance business and covers 15 countries on four continents.

How did the programme start?

In 2013 the multinational decided it wanted to work with multiple EB networks to give their local HR the choice of partners in their local market. The programme was renewed in 2016 and 2019. It’s running at a break-even rate (after all commissions) which is, of course, the purpose of a GRS programme.

Why has it been a success?

The programme has been a success for a few reasons:

- Data – having quality data, that has improved at every renewal, has helped to ensure that the portfolio has been priced effectively and helped reach that break-even success.

- Global vision – despite differing performance in some markets, the multinational looks at programme as a true global solution and understands that it’s about the global result and not being the cheapest in every local market.

- Collaboration – the client has worked closely with the EB network and the broker to ensure everyone is on the same page, has the right expectations and access to the data needed. Within the multinational, the collaboration between global HR and risk functions have ensured that local HR has the benefits they need to support their employee and risk is comfortable from the pricing standpoint.

What’s next?

When the programme started, the idea was to create a long-term, sustainable GRS programme – having now been in place for over seven years, the programme has done that. Now captives are becoming more common for financing EB, the multinational is exploring a potential move to a captive programme.

When the programme started, the idea was to create a long-term, sustainable GRS programme – having now been in place for over seven years, the programme has done that. Now captives are becoming more common for financing EB, the multinational is exploring a potential move to a captive programme.

The GRS programme has helped ready the client’s organisation for a captive solution, meaning they are more centralised and are experienced in making similar risk and underwriting decisions – the major difference is that they are not currently holding the risk.

GRS – a growth market for the right businesses

As multinationals look to control costs while continuing to offer the benefits that attract and retain the best talent, it’s no surprise that GRS has become more popular and more multinationals will continue to explore this option.

As Matthias Helmbold said: “In recent years we have seen more multinational employers and their global brokers interested in the advantages that GRS programmes provide, over and above a global pool. Over the last three years our GRS programmes have doubled, although they still are only a small number compared to our pools and captives. The main reason clients have gone down the GRS route is the desire to achieve a long-term sustainable solution using their centralisation and the global position of their portfolio.”

The COVID-19 pandemic has strengthened the argument for GRS, too. With the economic landscape changing now more than ever, there’s a need for multinationals to have a strong global benefits strategy providing benefits to care for their people and their dependents, while having a global governance structure and sustainable pricing.

So, what about the future of GRS? Are they here to stay? Matthias Helmbold says “yes”, but thinks it needs a strong partnership before implementation to make sure it’s a success.

“Looking ahead, we expect EB networks to continue working closely with global consultants to ensure that everyone understands who a GRS programme is right for, so that everyone’s expectations are met from the start. We’re actively trying to be very clear and transparent on what it needs to make these partnerships a success so they can be a long-term answer for centralised multinationals.”

This document has been prepared by MAXIS GBN and is for informational purposes only – it does not constitute advice. MAXIS GBN has made every effort to ensure that the information contained in this document has been obtained from reliable sources, but cannot guarantee accuracy or completeness. The information contained in this document may be subject to change at any time without notice. Any reliance you place on this information is therefore strictly at your own risk. This document is strictly private and confidential, and should not be copied, distributed or reproduced in whole or in part, or passed to any third party.

The MAXIS Global Benefits Network (“Network”) is a network of locally licensed MAXIS member insurance companies (“Members”) founded by AXA France Vie, Paris, France (AXA) and Metropolitan Life Insurance Company, New York, NY (MLIC). MAXIS GBN, registered with ORIAS under number 16000513, and with its registered office at 313, Terrasses de l’Arche – 92 727 Nanterre Cedex, France, is an insurance and reinsurance intermediary that promotes the Network. MAXIS GBN is jointly owned by affiliates of AXA and MLIC and does not issue policies or provide insurance; such activities are carried out by the Members. MAXIS GBN operates in the UK through UK establishment with its registered address at 1st Floor, The Monument Building, 11 Monument Street, London EC3R 8AF, Establishment Number BR018216 and in other European countries on a services basis. MAXIS GBN operates in the U.S. through MetLife Insurance Brokerage, Inc., with its address at 200 Park Avenue, NY, NY, 10166, a NY licensed insurance broker. MLIC is the only Member licensed to transact insurance business in NY. The other Members are not licensed or authorised to do business in NY and the policies and contracts they issue have not been approved by the NY Superintendent of Financial Services, are not protected by the NY state guaranty fund, and are not subject to all of the laws of NY. MAR718/1020