Captivated by Defined Benefit pensions

NEWS

Thursday 7 September 2017

London, UK

The use of captives to manage employee benefits liabilities is a well-established strategy used by multinationals. It helps to simplify the administration and costs of cross-border employee benefit (EB) programmes. The use of captive structures has also helped underpin the increasing focus on data and digital technologies driving next-generation EB schemes.

For instance, a recent qualitative global study1 commissioned by MAXIS Global Benefits Network found an increased appetite from EB consultants to promote captive and pooled arrangements. Consultants reported an uplift in the need for the central underwriting of risk, with multinational clients looking at solutions for upwards of 20 or 30 countries built on a single pricing structure.

One of the more significant developments over the past few years in the use of captives has been in helping corporations manage their liabilities from Defined Benefit (DB) pension schemes.

AXA, one of two shareholders in MAXIS GBN along with MetLife, is at the forefront of this market thanks to the firm’s extensive experience of captives, institutional asset management and reinsurance structures – all of which are required to succeed in this developing area.

A significant de-risking journey

It has been apparent for a long time that DB pension schemes are on a significant de-risking journey, looking to manage longevity risk in an era when investment returns and yields have fallen dramatically and scheme members are living longer than they ever have before. The options available to sponsors and trustees for reducing or removing this risk are bulk annuity transactions such as buy-ins or buy-outs; or longevity hedging/ swaps.

Let’s take the UK and its large DB market as an example. According to industry consultant Lane Clark & Peacock (LCP)2, the pensions de-risking market in the UK hit a key milestone in late 2016 with the pensions of over one million people insured through a buy-in or buy-out. Over the past ten years, UK company pension plans have transferred £70 billion of assets to insurers, said LCP, around 5% of the c. £1,500 billion of total DB pension assets.

LCP forecast that 2017 will be a record year for buy-ins and buy-outs of UK pension plans, with volumes for the first time hitting £15 billion.

LCP forecast that 2017 will be a record year for buy-ins and buy-outs of UK pension plans, with volumes for the first time hitting £15 billion.

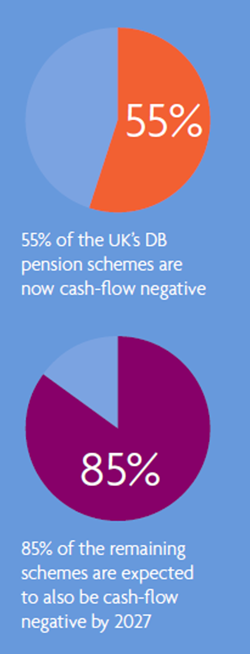

Other market surveys have underscored the reasons for the ever-increasing focus on de-risking. Some 55% of the UK’s DB pension schemes are now cash-flow negative, up from 42% last year, concluded Mercer’s recent European Asset Allocation Report 20173. It also found that 85% of the remaining schemes are expected to also be cash-flow negative by 2027, lacking sufficient income from investments and contributions to pay member pensions.

And a report4 last year from PwC said that the combined deficit of the UK’s 6,000 DB pension funds had grown to £710 billion. Schemes had total assets of around £1,450 billion but were liable to pay out about £2,160 billion in contractual promises. Clearly, something needs to be done.

AXA’s Defined Benefit solution is based on a buy-in strategy

AXA’s DB solution is based on a buy-in strategy in which sponsors pay AXA to take on some or all of the liabilities and all related risks. In an indication of the strong interest in this solution, AXA has already worked with a number of companies (pensions sponsors) in the UK and Ireland with regards to their DB liabilities.

Under the solution, the sponsor makes a one-off contribution to the scheme to plug any funding shortfall, and the scheme in turn enters into an annuity buy-in transaction. The insurance arrangement is then reinsured by a captive reinsurance vehicle owned by the sponsor themselves.

The potential benefits of using captive structures to mitigate DB risks include an increase on the return on assets with an investment policy, in line with long-term liabilities instead of a typically more conservative strategy set by the Trustees. They also offer the option to get any surplus out of the scheme in case of an increase of discount rates and/or an over-performance of the assets.

In addition, using a captive can ease governance with the Trustees, as asset management decisions are made within the captive and discussions with Trustees can focus on the scheme itself. Advantages for the captive include the ability to diversify the risk in the captive with longevity and market risks, and thanks to the diversification, the capital balance required by Solvency II can be reduced.

Capturing investment returns on premiums and reserves

The benefits of using captives in financing cross-border employee benefits are well established. From an economic perspective, for instance, they offer the ability to capture investment returns on premiums and reserves and the pension risk governance is centralised allowing for economies of scale. Moreover, the disposal of subsidiaries will be facilitated by eliminating any defined benefit legacy issue. In terms of data management, captives are also offering multinationals more transparency of overall global financial performance and the ability to improve claims and cost management by analysis of better claims data.

Given these sorts of benefits, the focus for many stakeholders is naturally turning to how captive structures can help manage other financial liabilities – with UK DB schemes firmly in the sights.

1 MAXIS GBN commissioned Charterhouse Research to conduct in-depth qualitative interviews with 32 senior employee benefits professionals working for multinational organisations, global employee benefits consultants, and local MAXIS GBN member insurance firms across territories in Asia, EMEA and the Americas, with fieldwork completed between 2 December 2016 and 20 March 2017.

2 https://www.lcp.uk.com/pensions-benefits/publications/lcp-pensions-de-risking-2016

3 http://www.theactuary.com/news/2017/05/half-of-db-pension-schemes-now-cash-flow-negative

4 https://www.theguardian.com/money/2016/sep/01/uk-defined-benefit-pension-fund-deficit-grows-100bn-one-month-pwc

The MAXIS Global Benefits Network (“Network”) is a network of locally licensed MAXIS member insurance companies (“Members”) founded by AXA France Vie, Paris, France (AXA) and Metropolitan Life Insurance Company, New York, NY (MLIC). MAXIS GBN, registered with ORIAS under number 16000513, and with its registered office at 313, Terrasses de l’Arche – 92 727 Nanterre Cedex, France, is an insurance and reinsurance intermediary that promotes the Network. MAXIS GBN is jointly owned by affiliates of AXA and MLIC and does not issue policies or provide insurance; such activities are carried out by the Members. MAXIS GBN operates in the UK through UK establishment with its registered address at 1st Floor, The Monument Building, 11 Monument Street, London EC3R 8AF, Establishment Number BR018216 and in other European countries on a services basis. MAXIS GBN operates in the U.S. through MetLife Insurance Brokerage, Inc., with its address at 200 Park Avenue , NY, NY, 10166, a NY licensed insurance broker. MLIC is the only Member licensed to transact insurance business in NY. The other Members are not licensed or authorised to do business in NY and the policies and contracts they issue have not been approved by the NY Superintendent of Financial Services, are not protected by the NY state guaranty fund, and are not subject to all of the laws of NY. MAR000xx/0817